Skip to content

Skip to content

Claiming Social Security is one of the most important — and permanent — financial choices you’ll make in retirement. At first glance, the decision might seem straightforward: collect early and get paid sooner, or wait and receive a bigger monthly check. But the truth is far more nuanced, and timing your claim wrong could cost you thousands in lost income and unnecessary taxes.

At IRSProb.com, we guide individuals and couples through the financial maze of retirement, helping them evaluate not just when to file, but how to make Social Security work in harmony with the rest of their tax and income strategy.

The Basic Rules: What Are Your Options?

You can start collecting Social Security as early as age 62, but your benefits will be permanently reduced. Alternatively, waiting until full retirement age (between 66 and 67, depending on your birth year) gives you your full benefit amount. Holding off until age 70 increases your monthly payout by up to 8% per year after your full retirement age, thanks to delayed retirement credits.

That sounds like a clear-cut incentive to wait, right?

Not so fast.

It’s About More Than Just the Monthly Check

There are four key factors that should guide your decision — and none of them should be ignored:

1. Longevity Expectations

If your family history and health suggest a longer-than-average life expectancy, delaying benefits can result in a greater total payout over time. However, if health concerns suggest otherwise, it might make sense to file earlier.

2. Current and Future Income

Are you still working in your 60s? Collecting benefits early while earning income can trigger the earnings test, which temporarily reduces your Social Security payout. Additionally, high earnings can push a portion of your benefits into the taxable zone.

3. Spousal and Survivor Benefits

Your decision doesn’t only affect you — it affects your spouse. In many cases, the higher earner’s choice has long-term implications for survivor benefits. Delaying benefits may ensure a larger payout for your spouse if you pass away first.

4. Taxes and Medicare Premiums

This is where most people overlook the true cost of filing early. Drawing Social Security alongside tax-deferred withdrawals (like from a 401(k) or IRA) can push you into a higher tax bracket, increase the taxability of your Social Security, and raise your Medicare Part B and D premiums.

How Strategic Timing Can Lower Lifetime Taxes

Here’s a common strategy we implement for clients at IRSProb.com:

Delay Social Security to 70, and in the meantime, use your early retirement years (60s) to draw strategically from your IRAs or other tax-deferred accounts. This reduces your account balances before Required Minimum Distributions (RMDs) begin at age 73, potentially lowering your tax liability later in life.

Not only does this smooth out your taxable income across retirement, it also helps avoid “tax torpedoes,” sharp spikes in income that can lead to higher Medicare costs and increased Social Security taxation.

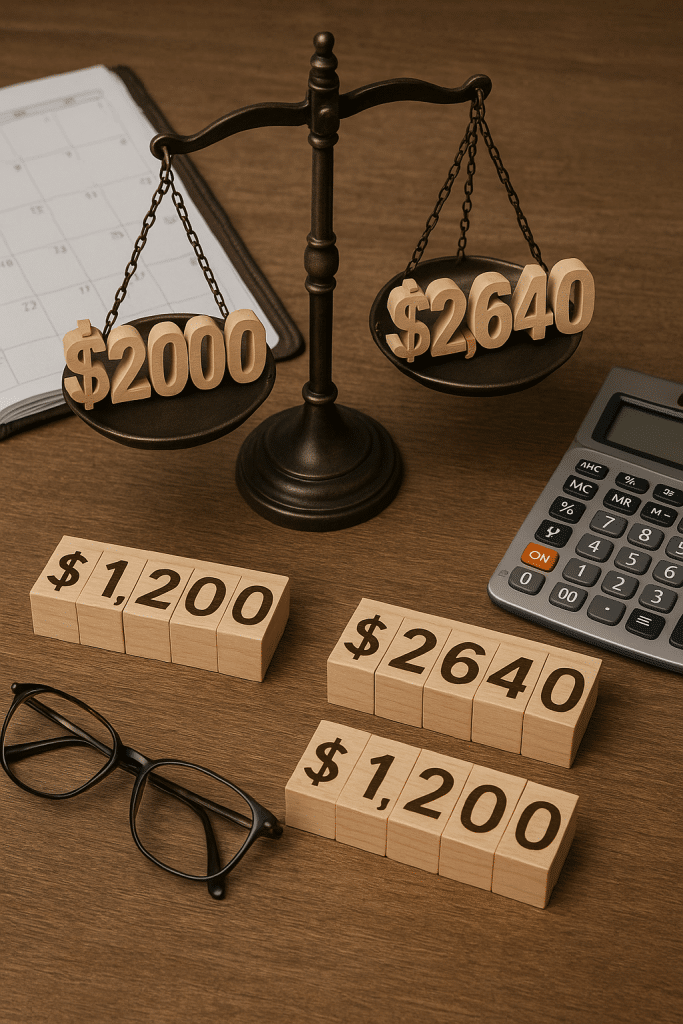

Case Study: A Married Couple’s Dilemma

Let’s say David and Linda are both retiring at 65. David is the higher earner and considering filing immediately. Linda has a modest work record but will qualify for spousal benefits.

If David claims at 65, he receives $2,000/month. If he waits until 70, his benefit grows to $2,640/month. More importantly, his delay increases Linda’s potential survivor benefit if he passes first, potentially the difference between her receiving $1,200/month or $2,640/month later in life.

By waiting, David and Linda not only secure more income but reduce Linda’s future financial risk.

Social Security Isn’t a Standalone Decision, It’s Part of a Bigger Picture

Choosing when to claim Social Security should never happen in a vacuum. This decision is deeply connected to the rest of your retirement plan — including how you draw from investment accounts, manage taxes, and structure your income for the long haul.

Rather than simply comparing early versus late filing, a more strategic approach looks at how this benefit interacts with your entire financial ecosystem.

That means asking the right questions:

- How will your Social Security income impact your tax bracket in retirement?

- Can delaying benefits reduce your reliance on taxable withdrawals early on — and smooth out required minimum distributions (RMDs) later?

- Will your filing decision affect a surviving spouse’s income or your eligibility for certain tax credits?

- Could filing at a certain age push you into a higher tier for Medicare premiums?

Taking these factors into account helps transform Social Security from just another retirement check into a powerful planning tool, one that can extend the life of your portfolio, reduce tax drag, and increase income flexibility over time.

The most effective strategies are coordinated, aligning Social Security with tax planning, healthcare costs, investment withdrawals, and legacy goals. When done right, this approach doesn’t just increase your monthly benefit, it enhances your total financial outcome over decades.

Final Thought: Don’t Just Guess — Get Professional Guidance

Making the right Social Security decision can easily add six figures to your retirement income over the years. But making the wrong choice can lock you into a suboptimal outcome forever.

That’s why IRSProb.com exists, to give retirees and pre-retirees a smarter, tax-aware strategy that integrates Social Security into a bigger, better financial picture.